UAE Corporate Tax 2026:

Rates, Deadlines & What Every Business Must Know

The UAE’s corporate tax regime has moved from a headline-grabbing introduction to full enforcement mode. In 2026, the Federal Tax Authority is auditing filings, issuing penalties, and tightening compliance expectations across mainland, freezone, and offshore entities alike. Whether you are running a business setup in Dubai, managing a freezone company, or expanding a multinational into the region, this guide covers everything you need to stay compliant and competitive.

What Is UAE Corporate Tax and Why It Matters in 2026

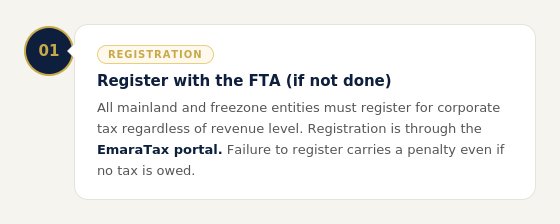

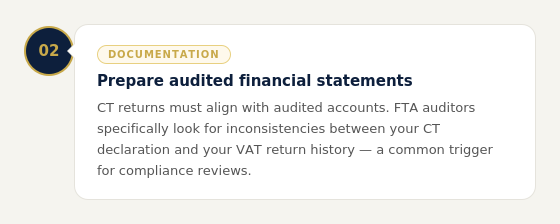

Introduced through Federal Decree-Law No. 47 of 2022 and administered by the Federal Tax Authority (FTA), corporate tax services in the UAE are no longer optional — they are a legal obligation for virtually every business. The first CT-liable period for calendar-year companies ran from 1 January 2024 to 31 December 2024, with returns due by 30 September 2025. In 2026, enforcement is intensifying: corporate tax is fully operational and enforcement is intensifying, with the FTA matching CT declarations against VAT returns and triggering audits on inconsistencies.

Understanding the corporate tax framework is now as fundamental to UAE business setup as choosing a trade license or a freezone jurisdiction. The right structure, setup, and compliance approach can mean the difference between a 0% effective rate and a 9% bill — plus penalties.

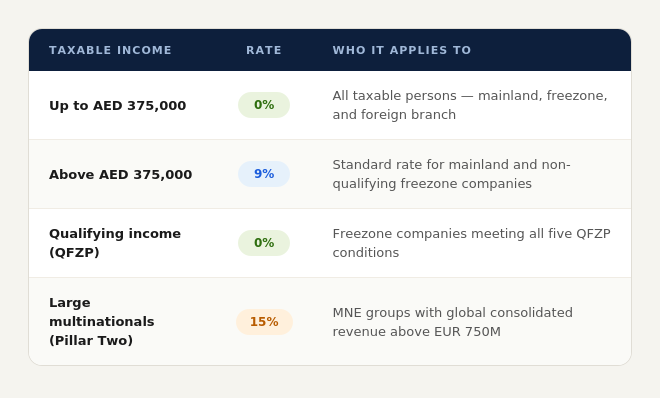

The Three-Tier Rate Structure

The UAE applies a straightforward rate structure — but the details matter enormously for company formation decisions and ongoing corporate tax services planning.

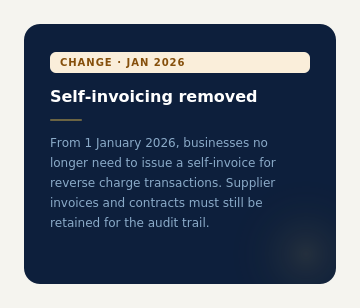

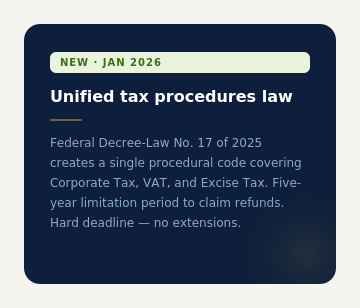

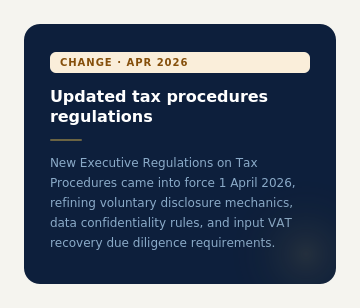

Key 2026 Regulatory Updates

Several significant changes came into force in late 2025 and early 2026, affecting every business registered with the FTA — from a Dubai free zone company setup to a large mainland company formation UAE.

Freezone vs Mainland: The Corporate Tax Reality in 2026

The relationship between freezone structures and corporate tax is now more nuanced than the simple “0% in freezone” narrative that preceded the CT regime. For anyone planning a Dubai free zone company setup or a mainland company formation UAE, the tax position must be modelled before — not after — the entity is formed.

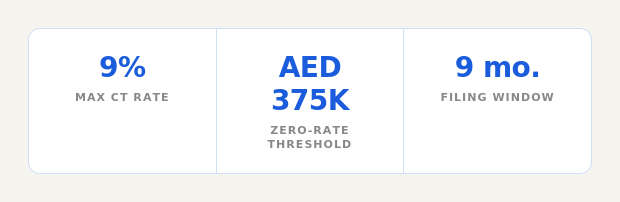

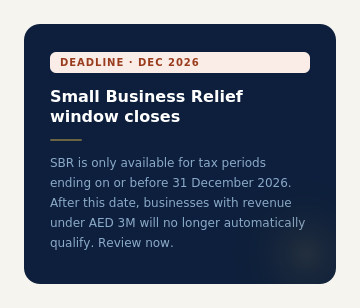

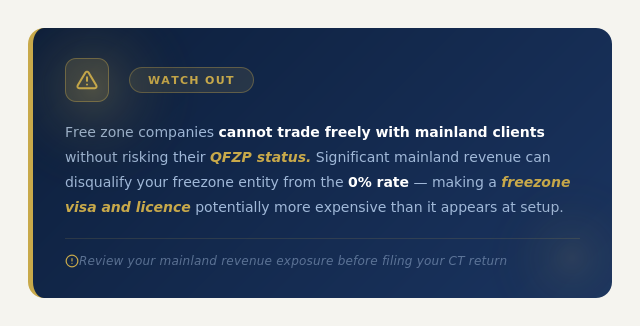

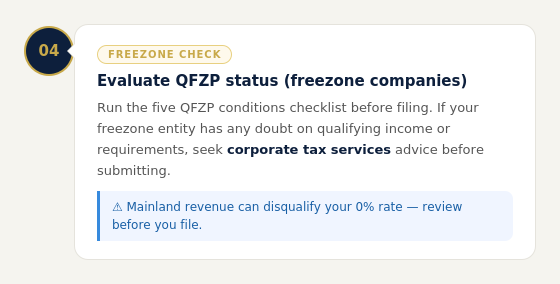

A freezone company qualifies for the 0% rate on qualifying income only if it achieves Qualifying Free Zone Person (QFZP) status by meeting all five conditions: adequate economic substance, qualifying income sources, the de minimis test on non-qualifying income, no mainland permanent establishment election, and arm’s-length pricing on related-party transactions. If it fails any condition, the 9% rate applies to taxable income above AED 375,000.

Meanwhile, a mainland company with taxable income below 375,000 AED pays exactly the same 0% CT as a fully qualifying freezone company, and also has full UAE market access. For many business setup in Dubai scenarios — particularly retail, hospitality, and local services — the mainland structure is actually the cleaner choice when corporate tax is factored in. A skilled corporate services provider will model both scenarios before advising on structure.

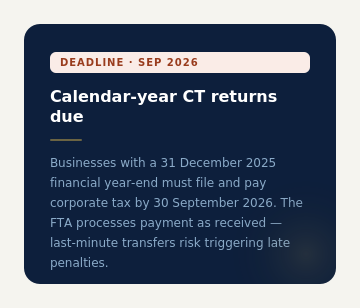

Filing Deadlines: What You Owe and When

The CT filing deadline is calculated from your financial year-end — not a fixed calendar date. The corporate tax return must be filed, and any tax due must be paid, within nine months from the end of the relevant financial year. A business with a financial year ending on 31 December 2025 must file and pay by 30 September 2026.

How Your Business Setup Choice Affects Your Tax Bill

For founders evaluating business setup services options, corporate tax services planning and entity structure are now inseparable. Here is how the main UAE business setup paths interact with the CT regime:

Mainland company formation UAE: Full UAE market access, no QFZP restrictions. Pay 0% on the first AED 375,000 of taxable income, 9% above. Ideal for businesses serving local clients, retail, hospitality, or those requiring a business license in Dubai for regulated activities. PRO services Dubai providers can assist with the FTA registration and ongoing compliance filings.

Free zone company setup: Potential 0% rate on all qualifying income if QFZP conditions are maintained. The freezone visa quota and flexi-desk options keep overhead low. However, the de minimis rule limits non-qualifying mainland income to the lower of AED 5 million or 5% of total revenue. Exceed this and you lose QFZP status for the entire period.

A corporate services provider with tax expertise — not just a business setup Dubai agent — is essential for navigating this distinction. The best approach is to run tax modelling before you apply for your business license UAE, not 18 months later when your first CT return is due.